Are you a new parent, or planning to be? Check out this financial guide to help guide you for the years to come:

http://www.nylinvestments.com/polos/RISWM86c-111558632.pdf

Your Custom Text Here

Are you a new parent, or planning to be? Check out this financial guide to help guide you for the years to come:

http://www.nylinvestments.com/polos/RISWM86c-111558632.pdf

by: Laura (Ciarkowski) McCarron

Director, Value Add Marketing, MainStay Investments

Personal loss is never easy. The death of a loved one can be one of the most emotionally trying periods in one’s life. And it is not uncommon for heirs to experience mixed emotions after receiving an inheritance—especially when it is unexpected. Many feel anxiety, stress, or even guilt over financially benefiting from a loved one’s death.

The funds were likely intended to bring a degree of financial security. But, because many do not know how to appropriately handle a sudden, large sum of money, some may find themselves financially worse off than before their inheritance. Heirs can stay in the right frame of mind after receiving a sizable amount of money with these tips

Whether expected or unexpected, losing a loved one is never easy. A trusted financial professional can be a valuable partner when it comes to navigating complex administrative and financial matters during a personally difficult time. He or she can also help heirs establish or realign their financial strategy and outline sound options for an inheritance.

Neither New York Life Investment Management LLC, its affiliates nor representatives provide tax, legal, or accounting advice. Please contact your own professionals.

The information and opinions contained herein are for general information use only. MainStay Investments does not guarantee their accuracy or completeness, nor does MainStay Investments assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice, and are not intended as an offer or solicitation with respect to the purchase or sales of any security or as personalized investment advice. There can be no guarantee that any projection, forecast, or opinion in these materials will be realized. Past performance is no guarantee of future results.

All investments are subject to market risk, including possible loss of principal. Diversification cannot assure a profit or protect against loss in a declining market.

Securities distributed by NYLIFE Distributors LLC, 30 Hudson Street, Jersey City, NJ 07302, a wholly owned subsidiary of New York Life Insurance Company. NYLIFE Distributors LLC is a Member FINRA/SIPC.

MainStay Investments® is a registered service mark and name under which New York Life Investment Management LLC does business. MainStay Investments, an indirect subsidiary of New York Life Insurance Company, New York, NY 10010, provides investment advisory products and services. This material is provided as a resource for information only. Neither New York Life Insurance Company, New York Life Investment Management LLC, their affiliates, nor their representatives provide legal, tax, or accounting advice. Please remind your clients to consult their own legal and tax advisors before implementing any plan.

1718543

Proactive investors know that the months before year-end are an ideal time to make any final tax-saving moves.

November 22, 2017

While keeping in mind your long-term investment goals, meet with your advisor and coordinate with your tax professional to examine nuances and changes that could impact your typical year-end planning.

Mind Your RMDs

Be thoughtful about required minimum distributions (RMDs) to ensure that you comply with the rules. If applicable and you have yet to do so, take your 2017 RMD to avoid a 50% penalty on required amounts not taken. Other considerations:

To Harvest or Not to Harvest

Evaluate whether you could benefit from tax-loss harvesting – selling a losing investment to offset gains or establish a deduction of up to $3,000. Excess losses also can be carried forward to future years. With your advisor, examine the following subtleties when aiming to decrease your tax bill:

Manage Your Income and Deductions

Those at or near the next tax bracket should pay close attention to anything that might bump them up and plan to reduce taxable income before the end of the year.

Evaluate Life Changes

From welcoming a new family member to moving to a new state, any number of life changes may have impacted your circumstances over the past year. Bring your financial advisor up to speed on major life changes and ask how they could affect your year-end planning.

Next Steps

Consider these to-dos as you prepare to make the most of year-end financial moves, and discuss with your financial advisor and tax professional:

Withdrawals prior to age 59 1/2 may also be subject to a 10% federal penalty tax. RMDs are generally subject to federal income tax and may be subject to state taxes. Consult your tax advisor to assess your situation. Raymond James advisors do not provide tax advice

As investors are faced with higher taxes, there are a few simple steps you can take to lower your tax bill.

November 22, 2017

Even in the wake of such complex tax provisions, a key to lowering your tax bill is really quite simple: Report lower taxable income. Since few of us actually want to earn less, the next option is to stash as much income as you can into tax-advantaged accounts. If you haven’t contributed the maximum amount to a qualified retirement plan at work throughout 2017, consider adding money before it is too late.

Your financial advisor can help develop a retirement account contribution strategy that works for your situation.

Photo by Nerthuz/iStock / Getty Images

Brian S. Wesbury, Chief Economist

Robert Stein, Deputy Chief Economist

Date: 10/30/2017

While tax cuts grab the headlines, the bigger issue for long-term economic growth is government spending. Tax receipts are above their long-term average as a share of GDP, but the government is still spending over $650 billion more than it takes in. And this government spending crowds out private sector growth.

Government spending since 2000 has risen from 17.6% of GDP (when the US had a surplus) to around 21% of GDP today. The more the government spends, the more it crowds out private sector growth and the slower the economy grows. It’s not that complicated.

Yes, tax cuts can help boost growth – at least temporarily – but without cutting spending, faster economic growth can’t be sustained, and eventually politicians will push tax rates back up in an attempt to pay the tab. Tax cuts are never “permanent” unless spending is contained.

We got into the current budget mess thanks to the 2009 jump in government spending as TARP and other supposed temporary stimulus programs added $535 billion to already excessive federal spending. This pushed spending as a share of GDP to 24.4% from 20.2% in a single year. But instead of unwinding that spending as the economy recovered from the financial crisis, government embraced Milton Friedman’s maxim that “nothing is as permanent as a temporary government program.”

As Friedman predicted, government spending never went back to its 2008, pre-crisis level of about $3 trillion per year. It flat-lined near $3.5 trillion over the next five years as the sequester helped contain it, but the sequester has since been scuttled and spending is now up to $3.98 trillion with the new 2018 budget, passed by the House and Senate, pushing it to $4.1 trillion.

Over recent decades, the US has never balanced its budget when spending was greater than 19.5% of GDP. As a result, unless tax cuts boost the economic growth rate high enough above the growth rate of spending, tax cuts will not have a long-term impact on GDP and living standards.

That said, two pieces of good news have developed in recent weeks. First, tax cuts seem to be on the way. Second, if the $4.1 trillion budget is passed, spending will be up around 3% from 2017, slightly slower than nominal GDP. This slower growth in spending paired with better policies should help the economy to accelerate in 2018 and drop spending to around 20.5% of GDP. But what if Congress and the President went one step further and froze spending at the current bloated level? As the included chart shows, if we make the conservative assumption that tax revenues remain near their historical 65-year average of 17.5% of GDP and if nominal GDP (real GDP plus inflation) grows only 3.5% annually – inline with the 3.6% annual growth rate over the past five years – with a spending freeze, the budget would balance in six years (2023). If fewer regulations and tax cuts boost nominal growth the budget would be balanced even sooner.

The last time we saw spending near 17.5% of GDP was in the early 2000’s. And, as you can see from the chart, revenues came in much stronger than their historical average. We don’t think this was a coincidence. A smaller government leads to a larger private sector. It becomes a virtuous cycle of faster growth, higher tax receipts and less need for government spending. Living standards would rise.

There is a lot of fat to trim within government. We believe if the private sector were running all of Washington, spending would fall drastically.

If President Trump passed a spending freeze, government would be forced to become more and more efficient. No more spending $283,500 on Department of Defense birdwatching, or nearly $150,000 to understand why politics stresses us out, or $65,473 to figure out what bugs do near a lightbulb. There are plenty of areas to cut excess…

But there are some issues that would need to be addressed with a spending freeze. First our military over the coming years is going to get bigger and stronger. Spending on defense will increase.

Second, what really drives a large part of government spending today is entitlements like Social Security, Medicare and Medicaid. With demographics and population growth, there is no question that these will continue to grow, but something needs to be done to bring down costs. It sounds trite, but we can even get inefficiencies out of entitlements, and we hope the Trump administration can help government think more efficiently.

As President Trump said in his inaugural address “… today we are not merely transferring power from one administration to another, or from one party to another –

but we are transferring power from Washington, D.C. and giving it back to you, the American People.” The best way to do this is by cutting the size of government. Freezing spending would be a big step in the right direction.

After all, from 1776, when the US was a backwater colony, to 1913, when it had become a leading power and would soon help save Europe in WWI, there was no Federal Reserve, or income tax. Government was much smaller. It’s time to shrink the burden of government and allow that magic of private sector growth to happen again.

Photo by vaeenma/iStock / Getty Images

Medicare’s open enrollment season is upon us. That means from now until December 7, you are able to make changes to your Medicare Advantage and prescription drug coverage. If you’re happy with your coverage, you don’t have to do anything. Even if you’re satisfied, open enrollment presents a great opportunity to make sure you’re getting the most out of Medicare.

Here are some tips to help you get started.

Medicare decisions can be complicated, but with the right tools and information, it doesn’t have to be. Raymond James is partnered with HealthPlanOne to provide you with personalized service, unbiased advice, and additional support from a dedicated licensed agent. There is no cost to use HealthPlanOne’s services and those services don’t end after enrollment. Your licensed agent will continue to provide support throughout the lifetime of your enrollment for coverage questions, appeals and plan renewals.

To learn more about HealthPlanOne, call the dedicated Raymond James number at 844-269-2646.

If you have any questions about open enrollment, or if you’d like to discuss how healthcare costs factor into your overall financial plan, please contact me so we can walk through the process together.

Please click on the link below to read an informational packet regarding your healthcare, retirement and choices:

https://myrjnet.rjf.com/MarketingMaterials/Marketing%20Materials/ALL/Whitepapers/Planning-Retirement-Healthcare-Wild-Card.pdf

Andrew Adams, CFA, CMT, Senior Research Associate discusses public company consolidation and its impact on investors.

October 20, 2017

Is the stock market experiencing a consolidation of power among a few of the largest companies, and if so, why?

The stock market is shrinking in terms of the number of publicly-traded companies, a fact that is both a result of, and contributing factor to, the increasing importance of a select few, large companies. Since 1996, the total number of listed stocks in the U.S. has been cut in half – from 7,322 to about 3,600 – as annual mergers and acquisitions have doubled and the average number of initial public offerings per year has dropped considerably. Meanwhile, the share of gross domestic product (GDP) generated by America’s 100 biggest companies rose from about 33% in 1994 to 46% in 2013 according to The Economist, meaning not only are there fewer firms in total these days, but a small number of them are taking a greater piece of the pie.

The concentration at the top is, of course, primarily weighted toward the big technology companies, all of which have seen their products and services become increasingly integrated into the lives of their loyal customers. Through innovation, acquisition and the power of so-called ‘network effects,’ these modern-day conglomerates have built dominant, industry-controlling brands that continue to gain value as their huge user bases expand. The digital age has witnessed data evolve into the most important commodity in the world, and much of the success of these large tech companies is due to the ever-widening ‘data moat’ that exists between them and up-and-comers lacking that established network of billions of existing customers.

Should investors and consumers be worried about the growing importance of mega-cap companies?

Despite the growing importance of these technology companies, the impact of the ten largest stocks in the S&P 500 has not really changed much over the last 40 years, even if the specific names on that list have changed. The ten biggest stocks currently make up a shade over 20% of the index’s market capitalization, which is right around the average since 1980 when the more cyclical energy sector helped the ten largest companies represent a dominating 25% of the S&P 500. Today’s large tech companies also happen to be some of the most profitable, with Apple, Google, Facebook and Microsoft alone accounting for about 10% of the S&P 500’s total profits. As such, technology’s place at the top of the market is not unwarranted. Moreover, the roughly 23% of the S&P 500 that technology represents today is nothing compared to the 34% it comprised back in March 2000 at the peak of the dot-com bubble. Considering American corporate profits (as a percentage of GDP) are higher than they have been any time since 1929, elevated valuations in the stock market are warranted and investors don’t appear overly concerned.

Consumers have also benefited in a big way, with technological innovation throughout history helping to bring down costs and prices, while making lives more convenient and requiring less manual labor. Per The Economist, tech companies provide Americans and Europeans with an estimated $280 billion-worth of “free” services per year, such as search results or directions. Even the stuff customers purchase provides tremendous bang for each respective buck. In their book Abundance, authors Peter Diamandis and Steven Kotler estimate that modern smartphones contain roughly $900,000 worth of applications based on each piece of technology’s original manufacturer’s suggested retail price in 2011 dollars (video conferencing, GPS, video camera, etc.), which illustrates the value being created by tech’s game-changing companies. It’s no wonder these disrupting forces are raking in the profits and the cash.

How are the big companies using all that cash?

The success of the mega-cap stocks has not only produced extraordinary profits, but it has also left the big tech companies with unprecedented levels of cash. As of June 2017, Apple, Alphabet, Microsoft, Amazon and Facebook together held $330 billion in cash (net of debt), and the S&P 500’s corporate cash as a percentage of current assets has basically doubled since 2000. Naturally, companies have had to find effective ways to use this cash; there has been a clear uptick in dividends, share buybacks, merger & acquisitions activity, and capital expenditures over the last several years. The share buyback policies have come under some criticism since they can help artificially boost earnings and sales per share numbers. However, buying back stock has been shown to help shareholders, and that is not the only way companies have been able to grow their businesses. The five aforementioned tech firms alone spent $100 billion last year on research and development (three times more than half a decade ago). These firms are definitely investing in the future. Finally, there is an estimated $2.4 trillion in cash held by U.S. companies overseas that is just sitting there not contributing much. Should tax reform occur next year and overseas cash comes home, Raymond James estimates share buybacks and the repatriated cash could improve S&P 500 earnings by an additional 1% - 2.5%.

https://www.raymondjames.com/branches/library/features/investment_strategy/investment_strategy.pdf

https://www.raymondjames.com/branches/library/features/investment_strategy/investment_strategy.pdf

The companies engaged in the technology industry are subject to fierce competition and their products and services may be subject to rapid obsolescence. Dividends are not guaranteed and will fluctuate. Past performance may not be indicative of future results. Investing involves risk including the possible loss of capital

Defend yourself with simple, everyday practices that can help protect your identity, your accounts and your devices.

October 20, 2017

Americans lose tens of billions of dollars each year to financial fraud. In the digital frontier, many crimes – including identity theft, tax fraud and elder abuse – are committed by online outlaws, making cybersecurity all the more important. As cybercrime becomes more prevalent, learn how to defend yourself with simple, everyday practices that can help protect your identity, your accounts and your devices.

Fighting Fraud

Familiarize yourself with common scams to help protect your assets and your identity. Often, identity thieves pretend to be someone they’re not, whether they’re claiming to be from a legitimate organization, acting as though they are in love or purporting to be someone you trust. The effort is an attempt to induce you to reveal personal information, such as passwords or credit card numbers. Crimes such as these fall under the umbrella of phishing, a popular fraudulent activity.

Never click on the unknown. If you receive an email from a reputable company, go directly to their website. If you receive an unexpected email from someone you know, call them before opening it. Additionally, never reveal your passwords and only use credit card numbers on sites you’re confident are secure. If you have any doubt, refrain from revealing personal information.

Tax season is a notable time to take extra precaution as email compromise and mail theft tend to crop up each year and more than 237,750 tax fraud victims are reported to the IRS annually. Remember that the IRS will never request personal or financial information by email, phone, text message or social media, nor will they threaten you with lawsuits, imprisonment or other enforcement action if you have done nothing wrong. Elect to receive your tax forms online rather than in your mailbox, where they may be at risk of physical theft, and file as soon as possible to decrease the likelihood that someone will maliciously file on your behalf.

Prudent Prevention

By taking small steps toward a safer online presence, you and your loved ones will be less likely to experience a loss of personal information and privacy. There are a number of everyday practices everyone should follow.

Post-Theft Protection

The Federal Trade Commission reports that 11.7 million people are victims of identity theft each year. Should your information be compromised, these are the actions you should take.

For more information on how to protect your self, please click on the link below:

https://www.raymondjames.com/pointofview/national_cyber_security_awareness_month

Talk to your advisor about these and other ways you can protect yourself and your accounts. Together, you can explore options like secure file sharing, fraud and consumer preference text alerts, and two-factor authentication.

Estate planning can feel overwhelming for individuals without children or close family members. Here are a few steps you should take, even in the face of uncertainty.

September 12, 2017

Estate planning can sometimes feel overwhelming for individuals without children or close family members. You may not know who should receive your estate, who should be the executor of your will, or whom you should trust with important decisions should you become incapacitated.

Not knowing the “perfect” way to craft an estate plan may lead you to do nothing at all – but this is a huge mistake, regardless of the size of your estate. Remember, if you pass away intestate, or without a will in place, your assets and property may fall to the direction of state statutes and the probate courts.

While estate planning can raise difficult questions – even for people with family ties and close friends – there are a few key decisions you should make right away, even in the face of uncertainty:

Choose an executor for your estate. Options exist beyond family members and friends, including lawyers, banks and other planning professionals. While making this choice can be difficult, your advisor can help with the decision, and he or she can also contact a Raymond James Trust consultant for additional support.

Create a living will. The document states your wishes should you be placed on life support or suffer from a terminal condition. Having it in place ensures that your physicians are aware of the action you want taken in the face of difficult end-of-life decisions.

Name a healthcare proxy or power of attorney. He or she will be tasked with making decisions about your health in scenarios not covered by your living will. As with your executor, you have the ability to ask a non-relative, such as a third-party professional or clergyperson, if they're willing to accept the responsibility. Note that your advisor can also help in selecting someone to act on your behalf if you become unable to tend to your finances.

Select beneficiaries for your 401(k) plans and life insurance policies. These won’t pass through your will, so you need to be clear about where you want your assets to go. Having trouble deciding who should receive your legacy? Think about your passions in life and consider tying your assets to charities for those causes. Your advisor can help you consider your options.

Having these decisions in place is an important first step to ensuring your estate is left the way you intend, regardless of familial ties – and be sure to review your selections regularly in case your circumstances change.

Raymond James financial advisors do not render advice on tax or legal matters. You should discuss any tax or legal matters with the appropriate professional.

Caregivers must perform a delicate balancing act — caring for their loved one and other family members, while also caring for themselves.

“These challenges often lead to emotional and physical stress as caregivers try to find a way to balance all of their caregiving duties and other life responsibilities,” says Amy Goyer, a caregiving expert for AARP.

America’s caregivers spend an average of almost 25 hours a week providing care for their loved ones, with almost one-quarter of those surveyed devoting at least 41 hours, a study by AARP and the National Alliance for Caregiving found. That can include helping loved ones perform daily activities, such as bathing, or they may provide medical care, such as giving injections or dressing wounds. What’s more: many caregivers do so without having received any training to help them handle those responsibilities, the study found.

As a result of those demands, “caregivers don’t care for themselves (and) their health really starts to suffer,” says Gail Hunt, president of the National Alliance for Caregiving, a nonprofit coalition of organizations working to improve the lives of caregivers.

In fact, 22% of the caregivers surveyed said their own health had declined since they began their caregiving duties, and 38% said their caregiving situation was “highly stressful.”

The demands of daily life often mean caregivers let their social life slide. “That means a lack of connections and a shrinking support system,” Goyer says. “We become isolated, which puts us at risk in all sorts of ways, including in terms of our health.”

Stress and exhaustion can also have a major impact. “We may become short-tempered, less patient, scattered and discouraged,” she says. “It’s hard to keep up a positive attitude and encourage those we are caring for when we are so depleted.”

Finding Strength in Support

With more than 43 million Americans providing care for a loved one1, caregivers should know they don’t need to soldier on alone, as resources are available to make their physical, emotional and financial lives easier.

Goyer recommends that caregivers take part in a support group, either online or in person, so they can draw on the knowledge and insights of others. While organizations like AARP offer a wide range of caregiver resources from self-care to legal and financial help, caregivers can find this kind of peer-to-peer support from Facebook groups that allow users to share experiences and insights to better equip them with assisting loved ones with specific illnesses, such as dementia.

Another important resource is the Eldercare Locator, provided by the U.S. Administration on Aging, which allows caregivers to find services that are available in their area.

For caregivers who work, or who want their loved one to have contact with others, adult day care may be an option, Hunt says, and fees are usually based on a sliding scale.

Caregivers also might be able to find respite care for their loved ones, so they are able to take a break, or can seek homemaker assistance, meal delivery and other services that can make caregivers’ lives easier, Goyer says.

One law designed to empower caregivers is the CARE (Caregiver Advise, Record, Enable) Act. Already adopted by 32 states and the District of Columbia, the measure is designed to help caregivers stay informed when a loved one is in the hospital, and to help them be better prepared to care for that person once he or she returns home.

Among other things, the act requires a hospital or rehabilitation facility to record the name of the caregiver when a loved one is admitted, and then notify the person when the patient is to be discharged. It also requires hospitals and rehabilitation facilities to provide information and instruction on medical tasks the caregiver will need to perform.

The Costs of Care

Along with the emotional and physical challenges, caregiving can also place heavy demands on a caregiver’s financial life, says Frank McAleer, vice president of financial planning and retirement solutions at Raymond James.

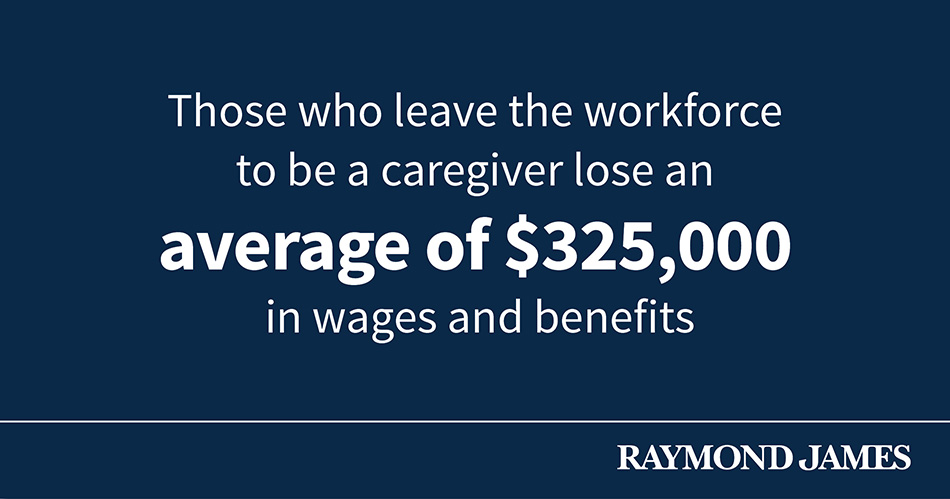

Those who leave the workforce to be a caregiver lose an average of $325,000 in wages1 and benefits, McAleer says. They also spend about $11,000 out of pocket each year to help care for their loved one.2

Even those who continue to work might have to cut back on their hours or skip a promotion in order to provide care, Goyer says.

The survey by the National Alliance for Caregiving and AARP found nearly one in five caregivers experienced financial strain.

That means it’s incumbent that individuals plan for the possible financial impact of caregiving. That planning typically needs to begin when clients are in their 50s, McAleer says.

But many people don’t want to admit their concerns, or know where to begin. To address that, McAleer educates Raymond James’ financial advisors on questions they can ask clients regarding any potential caregiving needs that could affect their financial plans.

The company has also made available guides to help clients navigate healthcare, caregiving, transportation and housing needs, both for loved ones now and for themselves in the future.

“One common theme is money,” McAleer says. “Caregivers often have to navigate financial topics with their loved ones, while also managing their own money.”

By proactively preparing a financial roadmap for such costs, caregivers are thus better positioned to combat any compounding stress that may contribute to their emotional and physical well-being.

1“Caregiving in the U.S.,” AARP, 2015

2“Study of Caregiver Costs to Caregivers,” Metlife, 2011

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Photo by Soft_Light/iStock / Getty Images

Domestic equity indexes ended August mostly flat, a contrast to the last several months of momentum. The end of the month saw geopolitical concerns arise between North Korea and Japan, and Brexit negotiations have not made notable progress. Yields on the 10-year U.S. Treasury slid, as investors sought safety Treasuries and gold.

In better news, recent data showed property values and home prices had gained ground, in part because of a shortage of inventory, a strong job market helping to increase demand and still-low mortgage rates. Consumer confidence also rose to its second-highest level since 2000, which bodes well for gains in consumer spending going forward, the largest part of the U.S. economy.

Market observers are also watching how Washington will deal with the looming showdown over the fiscal 2018 budget and the federal debt ceiling. While lawmakers are working toward a deal by the end of September, they can easily kick the can down the road, allowing more time to reach an agreement.

The major U.S. stock indices ended August largely mixed, with the S&P 500 and Dow essentially flat from the month before, the Russell 2000 down 1.39% and the Nasdaq up slightly at 1.27%. However, all are well into positive territory year-to-date.

Here’s a look at what else is happening in the economy and capital markets, as well as key factors we are watching:

Economy

Equities

International

Fixed Income

Bottom line

Please let us know if you have any questions about recent market events or how to position your long-term financial plan for the months ahead. We look forward to speaking with you.

Raymond James Financial Services does not accept orders and/or instructions regarding your account by email, voice mail, fax or any alternate method. Transactional details do not supersede normal trade confirmations or statements. Email sent through the Internet is not secure or confidential. Raymond James Financial Services reserves the right to monitor all email. Any information provided in this email has been prepared from sources believed to be reliable, but is not guaranteed by Raymond James Financial Services and is not a complete summary or statement of all available data necessary for making an investment decision. Any information provided is for informational purposes only and does not constitute a recommendation. Raymond James Financial Services and its employees may own options, rights or warrants to purchase any of the securities mentioned in this email. This email is intended only for the person or entity to which it is addressed and may contain confidential and/or privileged material. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information by persons or entities other than the intended recipient is prohibited. If you received this message in error, please contact the sender immediately and delete the material from your computer.

Photo by DNY59/iStock / Getty Images

We are proud of the accolades Raymond James continues to receive for its equity research. The recognition underscores the advantage of working with a firm such as Raymond James – one that values diligent analysis and prudent foresight.

This year, the Raymond James Equity Research department received 16 awards in the 2017 Thomson Reuters Analyst Awards for their stock selection and estimate accuracy on U.S. companies in industries ranging from information technology and communications to healthcare and pharmaceuticals. These awards are indicative of the deep industry knowledge, expertise and talent driving Raymond James Equity Research.

The firm now ranks fourth among all brokers in the U.S. and has been ranked in the top five in the U.S. over the past three- and five-year periods.

“Our Equity Research team works diligently to develop and share superior industry insight with our clients,” said Brian Alexander, director of Equity Research. “Our continued recognition from the Thomson Reuters Analyst Awards is further confirmation of the unprecedented expertise and ability behind our research.”

The Thomson Reuters Analyst Awards are recognized as the gold standard in objective measurement of sell-side analyst performance. Performance of analysts is measured in two ways: by the returns of their buy/sell recommendations and the accuracy of their earnings estimates. A detailed listing of methodology can be found on the Thomson Reuters Analyst Awards website.

If you would like to learn more about these awards, including how your portfolio may benefit from leveraging our award-winning equity research, please contact us any time.

Based on StarMine methodology, the Thomson Reuters Analyst Awards objectively measure the performance of analysts in two ways: by the returns of their buy/sell recommendations and the accuracy of their earnings estimates. The 2017 stock picking awards for the United States are based on the 2016 calendar-year performance of recommendations. The 2017 awards for estimating accuracy are based on quarterly periods that reported between April 1,2016 and 31 March 31, 2017. Only analyst performance on companies that are based in the United States is included in the awards calculations

Shine some light on these common misconceptions to help get the most from your hard-earned benefits.

July 25, 2017

Photo by IvelinRadkov/iStock / Getty Images

Reviewing the Quarter Ended June 30th, 2017

http://www.raymondjames.com/pdfs/capital_markets_review.pdf

Photo by uschools/iStock / Getty Images

Jeffrey D. Saut, Chief Investment Strategist,

"Washington, D.C."

So Andrew and I have been haunting my old stomping grounds here in the Washington, Baltimore, and Annapolis area while attending Raymond James’ national conference (The Summer Development Conference; SDC). We spent some time on Capitol Hill renewing long-term relationships and happened to run into our friend, and master economist for RSM (formerly McGladrey), Joe Brusuelas. I hate to admit this because I am pretty connected in this town, but Joe is better connected than me. Subsequently, I invited him to a dinner Tuesday night and he WOWWED about 20 of our financial advisors about what is going on inside the beltway, which is a mess! His comments reminded me of a quip from my deceased friend Ray DeVoe about one of the longest running plays in this town. To wit:

“There was one play that did have a lengthy run in Washington. J.M. Barrie's Peter Pan, starring Sandy Duncan as ‘The Boy Who Never Grew Up,’ which had the longest run at the time of any play produced in the nation’s capitol. In an interview, Ms. Duncan was asked why the play had lasted as long as it did. Her answer was, ‘I think it's because people in this town easily relate to fantasy.’”

And guess what, after having lived here for years in a past life, the current situation in D.C. does manifestly feel like “fantasy land!” And, that was the same feeling I got when I returned from some portfolio manager meetings yesterday and turned on the TV only to see m12 channels showing the O.J. Simpson parole hearings. I mean really, in a world overflowing with important news does anybody really care about an O.J. Simpson parole hearing, or as DJT calls it “fake news,” but I digress.

Returning to what the sagacious Joe Monaco writes “Rule #1; never mix your politics with your investment strategy!”

. . . Joe Monaco, Ph.D., captain of Norfolk, Virginia-Based Monaco Capital Management

https://raymondjames.bluematrix.com/sellside/EmailDocViewer?encrypt=45371c19-d539-40c1-9a0c-4a7be3a96c40&mime=pdf&co=RaymondJames&id=Matt.Goodrich@RaymondJames.com&source=mail

MarketWatch

Written by: Jillian Berman

America’s most popular major may also be one of the most lucrative.

Students who major in business, which for years has topped lists of most popular majors, earn between 81% and 130% more 12 years out of college than similarly talented students who don’t major in the field, according to a working paper distributed this week by the National Bureau of Economic Research, a Cambridge, Mass.-based research group

The study — based on wage and higher education data from Texas — looked at the earnings difference between students who just made the academic cutoff for being admitted to a school’s business major and those who just missed it. “A student who just barely makes the cutoff is pretty much identical to students who just barely miss it,” said Scott Imberman, an economics professor at Michigan State University and one of the authors of the study.

But students who just make the cutoff and choose to major in business “see very large earnings gains, in the order of pretty much doubling,” he said.

The findings come as the rising cost of college has pushed students to lean toward majors they think will help them find a decent-paying job. That strategy makes sense, given that a student’s choice of major may be a bigger factor in their life post college than where they choose to go to school. The difference in earnings over a lifetime between the highest and lowest paying majors is $3.4 million, according to a 2015 report from Georgetown University’s Center on Education and the Workforce.

It’s hard to say why exactly the researchers saw huge earnings gains for those students who chose to major in business, Imberman said. It could simply be because business as a field pays better, he said. But it’s also possible that students choosing to major in business are doing so because they know it fits their skill set and will, therefore, give them an advantage over others in the profession, he added.

Another interesting wrinkle: The greatest earnings gains were driven by the women who wound up majoring in business. Imberman said he and his co-authors couldn’t pinpoint why that’s the case, but they have some theories. The data indicates that it’s likely these women would have majored in a science, technology, engineering or math (STEM) field if they didn’t pursue business, which means they may have technical skills that would provide them with an advantage in business-related jobs.

“Alternatively, it could be that the STEM earnings for women are lower than those for men, but they equalize in business,” Imberman said, noting that that’s just a theory. STEM is notorious for its gender pay gap, but data indicates business has a large pay gap as well.

Though these women saw a big boost from their business major, betting on the field can be a bit tricky. The gap between the average annual earnings of the highest paying job for business majors and the lowest paying jobs in the field is about $25,000, according to the Georgetown Center. Business is also a field that’s often built on connections, so a business degree from a less prestigious university may not be a safe bet.

What’s more, employers are increasingly looking for students with communication and critical thinking skills. That’s put a premium over the past few years on liberal arts majors, who may be able to easily acquire the technical skills required for a business-related job.

Students should consider specifics instead of averages — like salaries and unemployment levels — when determining which major is best for them, Imberman said. His study indicates that students who are both interested in business and qualified to major in it are successful after they graduate, but that might not be true of a student who struggles with math or is interested in creative writing, but chooses to major in business anyway because they think it will be more lucrative

Photo by zimmytws/iStock / Getty Images

Kevin McGarry, Director for Nationwide Retirement Institute discusses how Medicare can impact your overall retirement plan

To see video, please click on the link below:

https://www.raymondjames.com/pointofview/planning-for-medicare-video?utm_source=hearsay&utm_medium=social&utm_campaign=retirement&utm_content=video

Photo by DNY59/iStock / Getty Images

Brian S. Wesbury – Chief Economist

Robert Stein, CFA – Dep. Chief Economist

Strider Elass – Economist

Remember the weak May payroll report – just 138,000? Didn’t think so. But, back then, that first report on May was reported as a massive economic slowdown that should stop the Fed from further rate hikes. But the weak May number was due to a calendar quirk that led to an undercount of college kids getting summer jobs. Payrolls jumped 222,000 in June, were revised up for May and, now, the two month average is 187,000. That’s exactly the same as the average in the past twelve months and almost exactly the same as the 189,000 average in the past seven years. In other words, the negative story from a month ago was misleading. So, guess what? The Pouting Pundits of Pessimism are pivoting! It’s not jobs anymore, now it is “high debt levels among nonfinancial corporations.” They say this happens near the very end of an economic expansion, so brace yourself. It is true that nonfinancial US corporation debt is at a record high of $18.9 trillion. It’s also true this debt is the highest ever relative to GDP. But these companies don’t pay their debt with GDP. They hold debt against assets and incomes. Since 1980, nonfinancial corporate debt has averaged 44.9% of total assets (financial assets, real estate, equipment, inventories, and intellectual property). Right now, these debts total 44.5% of assets, or slightly less than average. The record was 50.6 in 1993. Think about that, 1993 was right at the beginning of the longest economic expansion in US history.

Some say that the value of corporate financial assets is inflated by financial alchemy. So, let’s take financial assets, which include record amounts of cash, out of the equation. Before we do that, please realize that the financial assets of nonfinancial companies exceed total debts by $1.4 trillion, a record gap. But let’s look at ratios without them, anyway. The debt-to-nonfinancial asset ratio is at 85%. This is right in the middle of the past 25-year range – roughly 74% to 95%. Debt relative to the market value of these companies has averaged 82.2% since 1980 and currently stands at 80.0%. If you calculate net worth using historical costs for their nonfinancial assets (instead of market value), the debt-to-net worth ratio is 121%, but has averaged 128% since 1980, 125% since 1990, and 119% since 2000. Again, nothing abnormal. What about interest payments? The most recent data show that interest and miscellaneous payments are 11.2% of these companies’ profits versus an average of 13.2% since 1980, 12.2% since 1990, and 11.6% since 2000. What happens if interest rates keep rising? Less than you think. Only 28% of the debt is short-term versus an average of 44% in the 1980s, 41% in the 1990s, and 33% in the 2000s. None of this means the economy is safe forever. Another recession is inevitable. It’s just not coming anytime soon. In the meantime, beware of stories that take one simple measure – like corporate leverage – and spin it pessimistically.

http://www.ftportfolios.com/Commentary/EconomicResearch/2017/7/10/debt-laden-companies-fakenews

How to Avoid Splitting the Check Evenly When You Order Less Than Everyone Else

Jun 23, 2017

Photo by jacoblund/iStock / Getty Images

Friends afficionados will remember it well: Ross, Monica, and Chandler extravagantly eat beef carpaccio, grilled prawns, and Cajun catfish, while Joey, Rachel, and Phoebe, who are trying to save money, nibble on an appetizer-sized pizza, a side salad, and a cup of cucumber soup. When Ross splits the check, he says everyone owes $33.50. (This was 1995.) Phoebe pipes up, "uh-uh, no, sorry—not gonna happen. Sorry, but, cold cucumber mush for 30-something bucks? No. Rachel just had that little salad and Joey, with his teeny pizza. No." Her outburst inspires Ross to say they should each pay for what they had, but not without awkwardness.

Of course, while justified, Phoebe's pithy solution isn't the answer—but neither is breaking your bank to pay for a bottle of wine you didn't drink or an appetizer you didn't touch. So how do you deal with dividing a check over an inequitable meal?

If you know from experience that the dinner's organizer will likely encourage the other diners to simply split the check, you should be upfront with him before you even reach the restaurant, says Diane Gottsman, national etiquette expert, founder of The Protocol School of Texas, and author of Modern Etiquette for a Better Life. "Say, I'd love to join you, but I'm not the wine lover you are so I'm going to order separately," Gottsman suggests. No, it isn't the most comfortable conversation to have, but you won't be comfortable "stewing about the bill each time you go out, or building resentment towards your friends," she points out.

If you don't take this pre-restaurant proactive route, however, you still have options. When you sit down, consider letting your friends know you're on a tight budget, suggests Annette Harris, etiquette expert and founder of ShowUp! (However, Harris cautions, you shouldn't make this move if you're with your coworkers.) They may take your (not-so-subtle) hint.

You can also flag your server and say, "Please put my order on a separate check," Gottsman says. "The key here is to be preemptive—speaking directly to the server—and not making a big issue of your request." You can also try to make this arrangement before you walk into the restaurant, Harris says. "If you want to be discrete, call the restaurant in advance and ask the hostess if she could ask your server to split the check with your co-diner or diners."

Lastly, of course, you have an option to be a straight-shooter. Say something like, "Guys, I'm going to take care of my own tab. I don't have the same appreciation—or budget!—for your expensive bottles of wine," a short, to-the-point, and even light-hearted explanation your friends will understand, Gottsman says. "Some may follow your lead next time," she adds.

If you somehow get saddled into splitting the bill, there's not much you can do. "As the saying goes, you're a day late and a dollar [or way more] short," Harris says. "Trying to rectify the situation afterward is not a reasonable or realistic option." Think about it: do you really want to track down six dinner guests for the $1.30—or $8 total—they owe you? And "contacting the host to ask that they pay you the eight bucks might just damage your friendship or keep you off future invite lists," Harris says. "You have to ask is it worth it?"

Finally, remember: "There is nothing wrong with asking for your own check—as long as you do it upfront," instructs Gottsman. "When friends go out to dinner or drinks, unless you are clear, it's a given that most people will split the check and toss in their credit card at the end—which is perfectly fine, unless you're uncomfortable. Then it's up to you to take action in advance."

This article originally appeared in Foodandwine.com

With several financial deadlines behind you, take time this summer to review your progress, set new goals and tie up loose ends.

June 27, 2017

With several financial deadlines behind you, take time this summer to review your progress, set new goals and tie up loose ends. Tally up any recent life changes that may affect your estate plan, and adjust it as necessary. Evaluate your benefits and insurance.

Summer 2017 Market Closures

Tuesday, July 4: Independence Day

Monday, September 4: Labor Day

Planning To-Do's

Register with SSA.gov: This will allow you to check that your earnings history is accurate and to review expected benefits. If you are close to retirement age, begin a conversation with your advisor about when and how you should file to maximize your benefits.

Update your estate plan: Ensure that it protects you and your family in teh case of an unexpected event. Be sure to check the beneficiaries of your IRAs, insurance policies, trusts and any other accounts, and update any information that may no longer be relevant.

Review your benefits: Research your company's benefits and open enrollment schedule, and decide whether you need to make changes.

Review insurance needs: Periodically review and update coverage to ensure proper protection.

Address life changes: Speak with your advisor about any major changes that have occurred – marriages, births, deaths, divorces, a sudden windfall, etc. – and how they could affect your financial plan.

Download the complete checklist below and talk to your advisor to make sure you don't miss any important financial planning dates this summer.

A Plan for All Seasons: Summer 2017