Raymond James

Markets & Investing

September 30, 2024

The S&P 500 notched its first positive performance in a September since 2019.

September is typically the weakest month of the year for stocks, but thanks to the much-anticipated federal funds rate cut, the S&P 500 turned in its first positive performance in a September since 2019, achieving its 43rd record high of the year.

“The Federal Reserve [Fed] is recalibrating policy, and we are likely to see a series of rate cuts over the coming months as it gets closer to neutral, which is ultimately market friendly,” Raymond James Chief Investment Officer Larry Adam said.

The Fed took an unusual – but not entirely unexpected – step, cutting interest rates by 50 basis points (bps), rather than the usual 25, and is on track to successfully navigate a “soft landing” for the economy for the first time since 1995. The economy is showing resilience, the labor market remains stable, and inflation appears to be on a better path.

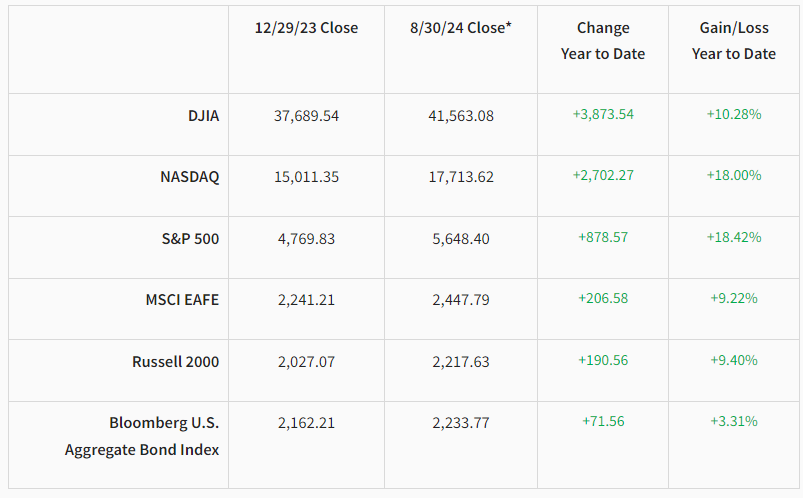

We’ll get into more detail shortly, but first, a look at the numbers year-to-date:

*Performance reflects index values as of market close on September 30, 2024. Bloomberg Aggregate Bond and MSCI EAFE reflect September 27, 2024, closing values.

U.S. economy continues to normalize

After last month’s surprising downward revision to employment numbers spanning from 2023 to early 2024, nonfarm payrolls for August were worse than expected at 142,000 new jobs – still strong compared to historical averages but a signal that the U.S. labor market is continuing to normalize. The job openings report was also lower than expected, and June’s numbers were revised lower, bringing job openings closer to pre-pandemic levels. At the same time, unemployment ticked down to 4.2% from 4.3% in July.

The services sector continued to expand in August, helping reduce market concerns about the strength of the U.S. economy. Manufacturing has struggled, but lower interest rates may help the sector out of its slump. Housing starts and building permits were higher than expected in August, and builders have accelerated completions, which increased by 9.2% from July to August and 30.2% year-over-year.

Market leadership broadens

While large companies continued to gain in value, small- and mid-size companies saw the strongest returns for the month, underscoring the importance of maintaining in a diversified portfolio. The Technology sector is still settling following its outsized performance earlier in the year, while interest rate-sensitive Utilities and Real Estate sectors are enjoying their time in the limelight. Two out-of-favor areas have perked up in the last week – Consumer Discretionary, thanks to the Fed’s rate cut, and Materials because of China’s strength due to policy measures intended to perk up the nation’s rocky position.

Long-term yields up, short-term down following rate cut

After the Fed’s September rate cut, the latest Federal Open Market Committee (FOMC) signaled an additional 50 bps in rate cuts by the end of the year and another 100 bps in 2025. Intermediate and long-term Treasury yields ultimately rose following the cut, steepening the curve. As expected, short-term yields fell in the leadup to the rate cut and in the days following: the one-year yield has fallen 73 bps since the beginning of August while the 10-year yield is down by just 21 bps. Bloomberg calculations are estimating 75 bps of cuts across the FOMC’s remaining two meetings this year.

Muni-to-Treasury ratios are near their highest levels of the year, with the 10-year ratio at about 70% and the 30-year around 85%.

Utility sector soars

As the Fed cut interest rates and the 10-year Treasury yield came down to 3.7% in September, investors began to feel more comfortable about companies that are more reliant on external funding. The Utility sector, which is famously rate sensitive, set an all-time high last month, surpassing the previous high from 2022. Utilities and independent power producers are also benefiting from the sentiment surrounding the AI boom given that the data center buildout is starting to provide a meaningful boost to electricity demand.

Important legislation excluded during "China Week"

While the House of Representatives spent significant energy on China-related policy earlier this month, several impactful and long-anticipated pieces of legislation were excluded from votes. Among them: provisions that would apply further scrutiny of U.S. investment into key Chinese tech, place new restrictions on data centers and reform the abilities of Chinese companies to import products into the U.S. duty-free via de minimis exemptions.

September also saw fears of a government shutdown averted, with Congress passing a compromise “clean” stopgap bill that funds the government through December 20. Legislators will now be directing their attention to the annual defense policy bill.

ECB cuts rates, UK holds steady

The European Central Bank (ECB) cut all key regional rates in September, a necessary move, according to President Christine Lagarde, because adjusted forecasts show inflationary pressures decelerating further over the bank’s two-year time horizon. Lagarde stressed that regional commercial bank lending conditions are still restrictive and expected to remain so for the near future. In contrast to the ECB, the UK’s Bank of England maintained the country’s base rate of interest at 5.0%, voting by a wide 8-to-1 margin not to loosen monetary conditions for the second time in as many meetings.

Following the backlash against its decision to raise interest rates in July, the Bank of Japan voted to not raise them again during its September rate-setting meeting.

The biggest news across international markets this month was the People’s Bank of China (PBoC) announcing broad stimulus measures in the country’s latest effort to halt persistent weakness in the real estate sector. The PBoC confirmed that it will set up a facility providing stockbroking firms, investment funds and insurance companies access to central bank liquidity specifically for the purchase of domestic equities.

The bottom line

While it’s good to see the broadening of the market and the lowering of interest rates excites investors, plenty of variables could spark volatility in the weeks and months ahead, including the health of the economy, employment and Fed messaging.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Raymond James Chief Investment Officer and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. Diversification does not guarantee a profit nor protect against loss. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australasia and Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small-cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges, which would reduce an investor’s returns. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification. A credit rating of a security is not a recommendation to buy, sell or hold the security and may be subject to review, revision, suspension, reduction or withdrawal at any time by the assigning Rating Agency. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Income from municipal bonds is not subject to federal income taxation; however, it may be subject to state and local taxes and, for certain investors, to the alternative minimum tax. Income from taxable municipal bonds is subject to federal income taxation, and it may be subject to state and local taxes. Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. The Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Studies. The Leading Economic Index (LEI) provides an early indication of significant turning points in the business cycle and where the economy is heading in the near term. This is not a recommendation to purchase or sell the stocks of the companies pictured/mentioned. Investing in small-cap stocks generally involves greater risks, and therefore, may not be appropriate for every investor. The prices of small company stocks may be subject to more volatility than those of large company stocks. The Nikkei 225 is a stock market index is for the Tokyo Stock Exchange (TSE). It is the most widely quoted average of Japanese equities. Sector investments are companies engaged in business related to a specific sector. They are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Material created by Raymond James for use by its advisors.