Shine some light on these common misconceptions to help get the most from your hard-earned benefits.

July 25, 2017

Your Custom Text Here

Shine some light on these common misconceptions to help get the most from your hard-earned benefits.

July 25, 2017

Photo by IvelinRadkov/iStock / Getty Images

Reviewing the Quarter Ended June 30th, 2017

http://www.raymondjames.com/pdfs/capital_markets_review.pdf

Photo by uschools/iStock / Getty Images

Jeffrey D. Saut, Chief Investment Strategist,

"Washington, D.C."

So Andrew and I have been haunting my old stomping grounds here in the Washington, Baltimore, and Annapolis area while attending Raymond James’ national conference (The Summer Development Conference; SDC). We spent some time on Capitol Hill renewing long-term relationships and happened to run into our friend, and master economist for RSM (formerly McGladrey), Joe Brusuelas. I hate to admit this because I am pretty connected in this town, but Joe is better connected than me. Subsequently, I invited him to a dinner Tuesday night and he WOWWED about 20 of our financial advisors about what is going on inside the beltway, which is a mess! His comments reminded me of a quip from my deceased friend Ray DeVoe about one of the longest running plays in this town. To wit:

“There was one play that did have a lengthy run in Washington. J.M. Barrie's Peter Pan, starring Sandy Duncan as ‘The Boy Who Never Grew Up,’ which had the longest run at the time of any play produced in the nation’s capitol. In an interview, Ms. Duncan was asked why the play had lasted as long as it did. Her answer was, ‘I think it's because people in this town easily relate to fantasy.’”

And guess what, after having lived here for years in a past life, the current situation in D.C. does manifestly feel like “fantasy land!” And, that was the same feeling I got when I returned from some portfolio manager meetings yesterday and turned on the TV only to see m12 channels showing the O.J. Simpson parole hearings. I mean really, in a world overflowing with important news does anybody really care about an O.J. Simpson parole hearing, or as DJT calls it “fake news,” but I digress.

Returning to what the sagacious Joe Monaco writes “Rule #1; never mix your politics with your investment strategy!”

. . . Joe Monaco, Ph.D., captain of Norfolk, Virginia-Based Monaco Capital Management

https://raymondjames.bluematrix.com/sellside/EmailDocViewer?encrypt=45371c19-d539-40c1-9a0c-4a7be3a96c40&mime=pdf&co=RaymondJames&id=Matt.Goodrich@RaymondJames.com&source=mail

MarketWatch

Written by: Jillian Berman

America’s most popular major may also be one of the most lucrative.

Students who major in business, which for years has topped lists of most popular majors, earn between 81% and 130% more 12 years out of college than similarly talented students who don’t major in the field, according to a working paper distributed this week by the National Bureau of Economic Research, a Cambridge, Mass.-based research group

The study — based on wage and higher education data from Texas — looked at the earnings difference between students who just made the academic cutoff for being admitted to a school’s business major and those who just missed it. “A student who just barely makes the cutoff is pretty much identical to students who just barely miss it,” said Scott Imberman, an economics professor at Michigan State University and one of the authors of the study.

But students who just make the cutoff and choose to major in business “see very large earnings gains, in the order of pretty much doubling,” he said.

The findings come as the rising cost of college has pushed students to lean toward majors they think will help them find a decent-paying job. That strategy makes sense, given that a student’s choice of major may be a bigger factor in their life post college than where they choose to go to school. The difference in earnings over a lifetime between the highest and lowest paying majors is $3.4 million, according to a 2015 report from Georgetown University’s Center on Education and the Workforce.

It’s hard to say why exactly the researchers saw huge earnings gains for those students who chose to major in business, Imberman said. It could simply be because business as a field pays better, he said. But it’s also possible that students choosing to major in business are doing so because they know it fits their skill set and will, therefore, give them an advantage over others in the profession, he added.

Another interesting wrinkle: The greatest earnings gains were driven by the women who wound up majoring in business. Imberman said he and his co-authors couldn’t pinpoint why that’s the case, but they have some theories. The data indicates that it’s likely these women would have majored in a science, technology, engineering or math (STEM) field if they didn’t pursue business, which means they may have technical skills that would provide them with an advantage in business-related jobs.

“Alternatively, it could be that the STEM earnings for women are lower than those for men, but they equalize in business,” Imberman said, noting that that’s just a theory. STEM is notorious for its gender pay gap, but data indicates business has a large pay gap as well.

Though these women saw a big boost from their business major, betting on the field can be a bit tricky. The gap between the average annual earnings of the highest paying job for business majors and the lowest paying jobs in the field is about $25,000, according to the Georgetown Center. Business is also a field that’s often built on connections, so a business degree from a less prestigious university may not be a safe bet.

What’s more, employers are increasingly looking for students with communication and critical thinking skills. That’s put a premium over the past few years on liberal arts majors, who may be able to easily acquire the technical skills required for a business-related job.

Students should consider specifics instead of averages — like salaries and unemployment levels — when determining which major is best for them, Imberman said. His study indicates that students who are both interested in business and qualified to major in it are successful after they graduate, but that might not be true of a student who struggles with math or is interested in creative writing, but chooses to major in business anyway because they think it will be more lucrative

Photo by zimmytws/iStock / Getty Images

Kevin McGarry, Director for Nationwide Retirement Institute discusses how Medicare can impact your overall retirement plan

To see video, please click on the link below:

https://www.raymondjames.com/pointofview/planning-for-medicare-video?utm_source=hearsay&utm_medium=social&utm_campaign=retirement&utm_content=video

Photo by DNY59/iStock / Getty Images

Brian S. Wesbury – Chief Economist

Robert Stein, CFA – Dep. Chief Economist

Strider Elass – Economist

Remember the weak May payroll report – just 138,000? Didn’t think so. But, back then, that first report on May was reported as a massive economic slowdown that should stop the Fed from further rate hikes. But the weak May number was due to a calendar quirk that led to an undercount of college kids getting summer jobs. Payrolls jumped 222,000 in June, were revised up for May and, now, the two month average is 187,000. That’s exactly the same as the average in the past twelve months and almost exactly the same as the 189,000 average in the past seven years. In other words, the negative story from a month ago was misleading. So, guess what? The Pouting Pundits of Pessimism are pivoting! It’s not jobs anymore, now it is “high debt levels among nonfinancial corporations.” They say this happens near the very end of an economic expansion, so brace yourself. It is true that nonfinancial US corporation debt is at a record high of $18.9 trillion. It’s also true this debt is the highest ever relative to GDP. But these companies don’t pay their debt with GDP. They hold debt against assets and incomes. Since 1980, nonfinancial corporate debt has averaged 44.9% of total assets (financial assets, real estate, equipment, inventories, and intellectual property). Right now, these debts total 44.5% of assets, or slightly less than average. The record was 50.6 in 1993. Think about that, 1993 was right at the beginning of the longest economic expansion in US history.

Some say that the value of corporate financial assets is inflated by financial alchemy. So, let’s take financial assets, which include record amounts of cash, out of the equation. Before we do that, please realize that the financial assets of nonfinancial companies exceed total debts by $1.4 trillion, a record gap. But let’s look at ratios without them, anyway. The debt-to-nonfinancial asset ratio is at 85%. This is right in the middle of the past 25-year range – roughly 74% to 95%. Debt relative to the market value of these companies has averaged 82.2% since 1980 and currently stands at 80.0%. If you calculate net worth using historical costs for their nonfinancial assets (instead of market value), the debt-to-net worth ratio is 121%, but has averaged 128% since 1980, 125% since 1990, and 119% since 2000. Again, nothing abnormal. What about interest payments? The most recent data show that interest and miscellaneous payments are 11.2% of these companies’ profits versus an average of 13.2% since 1980, 12.2% since 1990, and 11.6% since 2000. What happens if interest rates keep rising? Less than you think. Only 28% of the debt is short-term versus an average of 44% in the 1980s, 41% in the 1990s, and 33% in the 2000s. None of this means the economy is safe forever. Another recession is inevitable. It’s just not coming anytime soon. In the meantime, beware of stories that take one simple measure – like corporate leverage – and spin it pessimistically.

http://www.ftportfolios.com/Commentary/EconomicResearch/2017/7/10/debt-laden-companies-fakenews

How to Avoid Splitting the Check Evenly When You Order Less Than Everyone Else

Jun 23, 2017

Photo by jacoblund/iStock / Getty Images

Friends afficionados will remember it well: Ross, Monica, and Chandler extravagantly eat beef carpaccio, grilled prawns, and Cajun catfish, while Joey, Rachel, and Phoebe, who are trying to save money, nibble on an appetizer-sized pizza, a side salad, and a cup of cucumber soup. When Ross splits the check, he says everyone owes $33.50. (This was 1995.) Phoebe pipes up, "uh-uh, no, sorry—not gonna happen. Sorry, but, cold cucumber mush for 30-something bucks? No. Rachel just had that little salad and Joey, with his teeny pizza. No." Her outburst inspires Ross to say they should each pay for what they had, but not without awkwardness.

Of course, while justified, Phoebe's pithy solution isn't the answer—but neither is breaking your bank to pay for a bottle of wine you didn't drink or an appetizer you didn't touch. So how do you deal with dividing a check over an inequitable meal?

If you know from experience that the dinner's organizer will likely encourage the other diners to simply split the check, you should be upfront with him before you even reach the restaurant, says Diane Gottsman, national etiquette expert, founder of The Protocol School of Texas, and author of Modern Etiquette for a Better Life. "Say, I'd love to join you, but I'm not the wine lover you are so I'm going to order separately," Gottsman suggests. No, it isn't the most comfortable conversation to have, but you won't be comfortable "stewing about the bill each time you go out, or building resentment towards your friends," she points out.

If you don't take this pre-restaurant proactive route, however, you still have options. When you sit down, consider letting your friends know you're on a tight budget, suggests Annette Harris, etiquette expert and founder of ShowUp! (However, Harris cautions, you shouldn't make this move if you're with your coworkers.) They may take your (not-so-subtle) hint.

You can also flag your server and say, "Please put my order on a separate check," Gottsman says. "The key here is to be preemptive—speaking directly to the server—and not making a big issue of your request." You can also try to make this arrangement before you walk into the restaurant, Harris says. "If you want to be discrete, call the restaurant in advance and ask the hostess if she could ask your server to split the check with your co-diner or diners."

Lastly, of course, you have an option to be a straight-shooter. Say something like, "Guys, I'm going to take care of my own tab. I don't have the same appreciation—or budget!—for your expensive bottles of wine," a short, to-the-point, and even light-hearted explanation your friends will understand, Gottsman says. "Some may follow your lead next time," she adds.

If you somehow get saddled into splitting the bill, there's not much you can do. "As the saying goes, you're a day late and a dollar [or way more] short," Harris says. "Trying to rectify the situation afterward is not a reasonable or realistic option." Think about it: do you really want to track down six dinner guests for the $1.30—or $8 total—they owe you? And "contacting the host to ask that they pay you the eight bucks might just damage your friendship or keep you off future invite lists," Harris says. "You have to ask is it worth it?"

Finally, remember: "There is nothing wrong with asking for your own check—as long as you do it upfront," instructs Gottsman. "When friends go out to dinner or drinks, unless you are clear, it's a given that most people will split the check and toss in their credit card at the end—which is perfectly fine, unless you're uncomfortable. Then it's up to you to take action in advance."

This article originally appeared in Foodandwine.com

With several financial deadlines behind you, take time this summer to review your progress, set new goals and tie up loose ends.

June 27, 2017

With several financial deadlines behind you, take time this summer to review your progress, set new goals and tie up loose ends. Tally up any recent life changes that may affect your estate plan, and adjust it as necessary. Evaluate your benefits and insurance.

Summer 2017 Market Closures

Tuesday, July 4: Independence Day

Monday, September 4: Labor Day

Planning To-Do's

Register with SSA.gov: This will allow you to check that your earnings history is accurate and to review expected benefits. If you are close to retirement age, begin a conversation with your advisor about when and how you should file to maximize your benefits.

Update your estate plan: Ensure that it protects you and your family in teh case of an unexpected event. Be sure to check the beneficiaries of your IRAs, insurance policies, trusts and any other accounts, and update any information that may no longer be relevant.

Review your benefits: Research your company's benefits and open enrollment schedule, and decide whether you need to make changes.

Review insurance needs: Periodically review and update coverage to ensure proper protection.

Address life changes: Speak with your advisor about any major changes that have occurred – marriages, births, deaths, divorces, a sudden windfall, etc. – and how they could affect your financial plan.

Download the complete checklist below and talk to your advisor to make sure you don't miss any important financial planning dates this summer.

A Plan for All Seasons: Summer 2017

As June draws to a close, Mike Gibbs, Managing Director of Equity Portfolio & Technical Strategy, discusses earnings growth and current valuation levels.

June 27, 2017

The U.S. equity market remains on healthy footing, in our view. Earnings momentum is strong, economic conditions are okay, and competing assets offer paltry yields. The lack of progress on the headline political agenda has not been a setback as of now due to the exceptional earnings growth posted by the equity market in 1Q. We think the market is likely receiving a favorable boost by actions of the Trump administration to reduce regulatory constraints put in place by the Obama administration. Technically, the recent rotation (large cap tech into financials, industrials, and healthcare) is a healthy sign to us that investors are not eager to remove funds from the market when they book profits.

The market backdrop and our outlook remain positive; however, the S&P 500 has gained just under 20% over the past seven months. It is also trading at a valuation we view as full. These are two reasons influencing our opinion that the upside will be limited over the near term. We believe a basing period is likely to allow the market to digest the recent gains. In the process, the premium valuation should be lessened as earnings are expected to continue a healthy rate of growth. Also, investors should be given additional time to assess the potential of political success with the Trump agenda as well as analyze the health of the U.S. economy.

Absent any major setbacks economically (something we do not envision), any developing pullback periods are expected to be limited. Initial technical support levels near 2400 reaffirm the potential limited downside. Even in the case of a shift in investor sentiment to the negative, technical support levels just above 2300 (‐5%) suggest limited downside in the scope of normal market pullbacks. As a reminder, the average maximum annual drawdown for the S&P 500 since 1980 is 9% (excluding bear market years).

Articles are chosen for summary in this Market Intelligence blog based on newsworthiness in conjunction with The Infinite Loop themes. Any opinions and views expressed in the articles are generally those of the underlying author from the source listed, are not necessarily current as of the date of this blog, may change as market or other conditions change, and may differ from views expressed by Ivy Investment Management Company and its associates or affiliates. Actual investments or investment decisions made by Ivy Investment Management Company and its affiliates will not necessarily reflect the views expressed in the articles. These articles are distributed for educational purposes only and are not investment advice or a recommendation to purchase, sell or hold any specific security mentioned in the article or to engage in any investment strategy. Investment decisions should always be made based on each investor’s specific financial needs, objectives, goals, time horizon and risk tolerance. Securities discussed may not be suitable for all investors.

Photo by m-gucci/iStock / Getty Images

Chief Economist Dr. Scott Brown, Chief Portfolio Strategist Nick Lacy and Chief Investment Strategist Jeff Saut provide their in-depth views on the current and future state of the market and economy

To see video, please click on link below:

http://www.raymondjames.com/pointofview/a-look-at-whats-ahead-video?utm_source=hearsay&utm_medium=social&utm_campaign=marketupdates&utm_content=article

First Trust

Brian S. Wesbury, Chief Economist

Robert Stein, Dep. Chief Economist

The Federal Reserve did what almost everyone expected today, raising the target range for the federal funds rate by 25 basis points to 1.00% - 1.25%.

Here are the key takeaways from today’s statement from the Fed, its updated forecasts, its plan on reducing the balance sheet, as well as Fed Chief Yellen’s press conference.

First, although the market consensus is that the Fed isn’t going to raise rates again until 2018, the Fed thinks we still have one more hike in 2017, with the odds of two hikes equal to the odds of none at all.

Second, the Fed has a concrete plan to start reducing the size of its bloated balance sheet, a plan it is likely to start later this year. Once implemented, for the first three months, the Fed will reduce its balance sheet by $10 billion per month ($6 billion in Treasury securities, $4 billion in mortgage-related securities). Then, every three months, the amount of monthly balance sheet reduction will rise by $10 billion (w/ the same 60/40 proportion between Treasury securities and mortgage-related securities). That escalation will continue until the Fed is cutting its balance sheet by $50 billion per month.

Third, compared to three months ago, the Fed is expecting a little more economic growth this year, less unemployment, and less inflation. However, projections for economic growth and inflation remain unchanged beyond this year. The only significant change in the forecast was that the Fed now thinks the jobless rate will average 4.2% in 2018-19 instead of 4.5%. In addition, the Fed thinks the long run average rate for unemployment is 4.6% versus a prior estimate of 4.7%.

Fourth, the Fed is not impressed by the recent softness in inflation and does not think that softness is a reason to change the projected path of monetary policy. Although the Fed acknowledges inflation has receded back below its 2% target and is “monitoring inflation developments closely,” it thinks inflation will head back to 2% in the medium term.

Fifth, the Fed is no longer as concerned about the potential negative influence of foreign events, having removed language saying it was closely monitoring “global economic and financial developments.”

We still think the most likely path is that the Fed makes no policy changes in July but then uses the September meeting to make its last interest rate hike of the year while also announcing balance sheet reductions will start October 1. This is our interpretation of Yellen saying the balance sheet reductions would start “relatively soon.” A less loose monetary policy than the market consensus believes is, in part, why we think long-term Treasury yields will be moving up significantly later this year, with a 3.00% target for the 10-year Treasury Note by the end of the year.

The most disheartening part of the today’s Fed releases was that the plan for reducing the balance sheet noted that the Fed stands ready to use quantitative easing again in the future when the economy gets weak. We don’t think QE helped the economy and had been hoping the Fed had learned that lesson. Apparently not.

Overall, however, we are pleased the Fed raised rates today and look forward to another rate hike and the beginning of balance sheet reductions later in 2017. Neither of these will hurt the economy and will help prevent future problems that could.

Text of the Federal Reserve's Statement:

Information received since the Federal Open Market Committee met in May indicates that the labor market has continued to strengthen and that economic activity has been rising moderately so far this year. Job gains have moderated but have been solid, on average, since the beginning of the year, and the unemployment rate has declined. Household spending has picked up in recent months, and business fixed investment has continued to expand. On a 12-month basis, inflation has declined recently and, like the measure excluding food and energy prices, is running somewhat below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, and labor market conditions will strengthen somewhat further. Inflation on a 12-month basis is expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee's 2 percent objective over the medium term. Near term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1 to 1-1/4 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee currently expects to begin implementing a balance sheet normalization program this year, provided that the economy evolves broadly as anticipated. This program, which would gradually reduce the Federal Reserve's securities holdings by decreasing reinvestment of principal payments from those securities, is described in the accompanying addendum to the Committee's Policy Normalization Principles and Plans.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Patrick Harker; Robert S. Kaplan; and Jerome H. Powell. Voting against the action was Neel Kashkari, who preferred at this meeting to maintain the existing target range for the federal funds rate.

This report was prepared by First Trust Advisors L. P., and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable.

This report was prepared by First Trust Advisors L. P., and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

The information presented is not intended to constitute an investment recommendation for, or advice to, any specific person. By providing this information, First Trust is not undertaking to give advice in any fiduciary capacity within the meaning of ERISA and the Internal Revenue Code. First Trust has no knowledge of and has not been provided any information regarding any investor. Financial advisors must determine whether particular investments are appropriate for their clients. First Trust believes the financial advisor is a fiduciary, is capable of evaluating investment risks independently and is responsible for exercising independent judgment with respect to its retirement plan client

The Wall Street Journal

Maddy Dychtwald

Published: June 8, 2017 8:58 a.m. ET

Adult children accustomed to having Mom and Dad give them $200 here, $500 there may be in for a rude awaking. Cutting the children off is high on the list of actions parents are willing to consider to shore up their own retirement nest eggs.

In our most recent study, Finances in Retirement: New Challenges, New Solutions, we asked Americans which trade-offs and course corrections they’d be willing to make for a range of life priorities. When it comes to family, the top two actions people said they would be willing to consider are to “educate family on ways to be more financially independent” and to “cut back on financial support to children.”

Specifically, 84% of those surveyed said they would like to educate their family on ways to be more financially independent, while 70% said they would consider cutting back on support to postcollege children.

Having to live off of what you earn and live within your means may be one of the best lessons in life a parent can offer an adult child.

Among those Americans who give their adult children postcollege financial support, the average amount given is $6,800 annually, according to the study, a four-year, 50,000-respondent investigation into the changing lifescape of retirement conducted by my firm, Age Wave, in partnership with Merrill Lynch. And parents are gifting that money just as they are facing their own retirement head on.

If that money were, instead, invested in their own retirement, it could really add up. Redirecting the money could also empower young adults to be financially independent and help free them from the possible burden of helping their parents out financially later in life, if those parents didn’t save enough for retirement.

Consider a 50-year-old couple with a 22-year-old son just finishing college who plan to work until age 65. If they stop giving him, that, say, annual $6,800-per-year in financial support and instead set the sum aside for retirement, they’ll end up with an additional $102,000 in their retirement pot. And that’s if they just set the money aside. The amount could be larger if they invest the money and factor in any investment returns, compounding or interest.

But what about their son? What is the cost to him? It’s true that financial help might make his transition to adult life easier in the short run. But this is a critical time to build confidence in a variety of parts of life, including around money management. Having to live off of what you earn and live within your means may be one of the best lessons in life a parent can offer an adult child. Rather than enabling, we are empowering.

Our study also uncovered Americans’ greatest fear about retirement as it relates to family: being a burden on family members as we age. Sixty percent of middle-aged and older Americans said that was one of their greatest worries. When asked what it means to be a burden, they said they’re worried not only about needing physical care, but also about interfering with the lives, finances and emotional well-being of family members.

Supplementing our young adult children might seem like a huge help to them now. But in the long run, perhaps the greatest financial gift we can give them is to be able to afford our own retirement and the possible need for care in retirements that can last 30 years or more. The last thing many of us want is to have to turn to our children for financial help in their 40s or 50s — when they will be focused on paying mortgages, saving for their children’s college fund and funding their own retirements.

First Trust Monday Morning Outlook

Brian S. Wesbury – Chief Economist

Robert Stein, CFA – Dep. Chief Economist

Strider Elass – Economist

When the Federal Reserve raises rates by another quarter percentage point on Wednesday, you’re going to see many stories about monetary policy getting tight and the potential threat that poses for the economy in general and the bull market in stocks in particular. As usual, you should discount the conventional wisdom. What’s really going on is the Fed is getting “less loose,” not “tight” and there’s ample room for the Fed to stay along this path without risking a recession or a bear market.

The banking system is full of excess reserves from the Fed. Until the Fed eliminates those excess reserves or lifts the rates it pays banks on those reserves above the rates on loans, policy will remain loose. We expect the Fed to stay on track for a third rate hike in 2017. The Fed's “dot plots” indicate the odds of this are much higher than the market consensus that another rate hike later this year is only a 50-50 proposition. In addition, we expect both the Fed’s statement as well as Fed Chief Yellen’s press conference to keep it on course to start unwinding its bloated balance sheet later this year. Our best guess is another rate hike in September followed by six months of balance sheet reductions before rate hikes start again in

March 2018. However, we wouldn’t be surprised if the Fed embarked on balance sheet reductions a little earlier while moving a September rate hike to December. Either way, the Fed would be moving in the right direction. Some critics, however, are saying inflation and wages aren’t rising fast enough to justify rate hikes, which means the Fed should stand pat after Wednesday. But that reads too much into a few months’ worth of data. Even if consumer prices dipped 0.1% in May, the CPI would be up 1.9% from a year ago, a sharp increase from a 1.0% gain in the year ending in May 2016 and no change in the year ending in March 2015. In other words, the trend is still up.

Although average hourly earnings are up only 2.5% from a year ago, that figure includes many highly productive Baby Boomers retiring while lower productivity Millennials enter the workforce. The Atlanta Fed adjusts for demographics and finds underlying wage growth closer to 3.5% instead. We don’t mind faster wage growth and don’t think it causes inflation. But key policymakers at the Fed do, and in this case it will help lead them to the right policy, even if, in part, for the wrong reason.

Please click on the link below to see more:

http://www.ftportfolios.com/Commentary/EconomicResearch/2017/6/12/less-loose

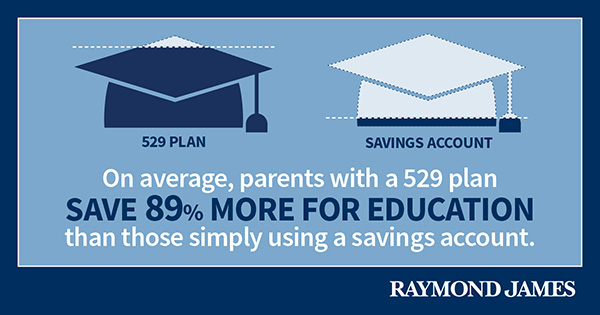

529 education savings plans are more versatile than you may think.

May 24, 2017

Many parents and grandparents start investigating their college savings options before a new addition to the family is even born. Why? Possibly because education is a top priority for their families, and already-expensive tuition increases almost 5% every year, according to The College Board. A child born in 2016 can expect to pay anywhere from $94,800 (public) to $323,900 (private) in tuition and fees for a four-year education in 2034, when he or she turns 18. However, saving toward that goal is much more achievable if you use the tools at your disposal wisely, particularly tax-advantaged college savings vehicles.

Not everyone is in a position to set aside money for the next generation without jeopardizing their own goals, but if you're fortunate enough to do so or if you can start early and save over time, it is worth looking into your options. Specialized savings accounts, informally referred to as 529s, should be at the top of your list because they offer preferential income and/or estate tax treatment. In fact, according to Sallie Mae's "How America Saves for College 2015," parents with a 529 plan save 89% more than those simply using a savings account. Here are a few advantages that parents and grandparents may want to consider.

57% of parents save for college, but most of that money is held in general savings accounts, not tax-advantaged educational savings vehicles.

Source: Sallie Mae's “How America Saves for College 2016”

Assets contributed to a 529 on behalf of your designated beneficiary grow tax-free. Even better? The withdrawals are tax-free as long as they're used for a qualified education expense, such as tuition, room and board, and supplies, and don't exceed the actual costs.

Most 529s are state-sponsored, which could provide additional tax savings. For example, some states offer a tax benefit to residents who invest in their state's plans. Others allow a state income-tax break if you contribute to any state's plan. It's important to understand which tax deductions or tax credits may be available– especially if you reside in a state with income tax. Your advisor can help you compare potential deductions.

Take Advantage of Flexibility

Many people worry that gifting large chunks of money to a 529 means they'll irrevocably give up control of those assets. Hard to swallow, when you've worked hard to build your net worth and can't predict if you'll need that money later. The good news is that 529s allow quite a bit of control, especially if you title the account in your name. At any point, you can get your money back. Of course, that means it becomes part of your taxable estate again, subject to your nominal federal tax rate, and you'll have to pay an additional 10% penalty on the earnings portion of the withdrawal if the money isn't used for your designated beneficiary's qualified higher education expenses.

What if your beneficiary receives a scholarship or financial aid? Well, you've got options here, too.

Plus, many plans offer you diversified portfolios allocated among stocks, bonds, funds, CDs and money market instruments, as well as age-based portfolios that are more growth-oriented for younger beneficiaries and less aggressive for those nearing college age.

Bypass Gift Taxes for Five Years

A grandparent, or anyone really, can contribute up to $14,000 a year per person ($28,000 if married filing jointly, for 2017) with no gift tax consequences. Better yet, if you can swing it, you can “super fund” your 529 using the five-year accelerated gift election, a lump sum gift of $70,000 per contributor ($140,000 for married couples). The catch here is that you can't make additional gifts for the next five years, but your larger gift now has the opportunity to compound tax-free over a longer time.

Minimize Potential Estate Taxes

Estate tax benefits can be significant, especially if you have a large number of kids or grandkids you want to benefit. Once a 529 plan is funded, it is considered a completed gift to the beneficiary for federal estate tax purposes even though the owner retains full control of the account. It shifts assets out of your estate (unless you make yourself the beneficiary) and can grow tax-free until needed. If opting for a five-year election, the contributor must outlive the election or it will be prorated back on a calendar year basis.

Give Generously

Lastly, it doesn't matter how much you make, you can contribute to a 529 for anyone of any age, including yourself if you plan to go back to school. And lifetime contributions are generous as well. Depending on the state, you can contribute more than $200,000 to help your future learner avoid or minimize student debt.

What About Financial Aid?

Most Americans supplement their contributions to college expenses with financial aid of some sort, but aren't quite sure how college savings could affect future aid. There are some things to consider with 529s. You have to decide how to title the account – who will own it and who will be the beneficiary. Is it better to own the 529 plan and make your child or grandchild the beneficiary or to put the 529 plan in the beneficiary's name outright? Another option for grandparents and aunts and uncles is to contribute to an existing 529, opened and owned by the child's parents.

Did you know?

You can avoid gift taxes altogether if you make tuition payments directly to a higher education institution even after you've reached your annual federal gift-tax exclusion limits. Doing so doesn't chip away at your lifetime gift exemption either, but it is likely to adversely affect financial aid applications.

The difference is how the distributions will be treated when it comes to seeking financial aid using the common Free Application for Federal Student Aid (FAFSA) form. The FAFSA form is the key to unlocking some portion of $150 billion in available federal tuition assistance. No reason to leave money on the table if it could be better deployed to achieve your own goals, right? These decisions can be complicated, and your financial advisor should be able to offer some helpful advice beyond the basics offered below.

If the 529 is owned by the parents

In this case, 5.64% of the assets in the 529 plan will be counted toward something called the Expected Family Contribution (EFC). That amount is recalculated each year based on the end value of the account, which will steadily decline since funds will be used to pay for education expenses. If the student owns the account, 20% of the balance counts toward the student's expected contribution. That's the case for any student-owned assets, so it's important to title assets appropriately.

If the 529 is owned by anyone but the beneficiary

Technically, if the account is owned by someone other than a custodial parent or student, such as a grandparent, it is not counted for financial aid purposes. However, the distributions are. FAFSA treats the distributions as the student's income – even if it's a qualified tax-free distribution for income-tax purposes, so this has the potential of limiting the value of your gift. However, this may be avoided by delaying 529 distributions until after the student has completed his or her FAFSA application for their junior year or later. FAFSA calculations consider income from what's called the prior-prior year – for the 2017-2018 FAFSA that would mean using your 2015 tax return – so the income from distributions won't be a factor toward the end of a college career.

Not every institution relies on the federal financial aid form. Some use the CSS/Financial Aid Profile from The College Board instead, which reports and treats 529 assets as available assets, regardless of how they're owned.

The Free Application for Federal Student Aid, known as FAFSA, is the first step to receiving your share of $150 billion in loans, grants and work-study funds for college or career school

Set Your Course Now

Saving for college doesn't have to be daunting, just disciplined. It helps to take advantage of investment vehicles designed to help you along the journey. Each has its benefits and considerations, so it's wise to talk to your professional advisor before making a years-long commitment. For example, 529s, like many other investments, come with fees and are subject to market fluctuations, unless you opt for a prepaid account. And you can only make changes to your asset allocation twice a year.

On the plus side, 529s have higher contribution limits, no income limits and a low impact on financial aid eligibility. They allow for tax- and penalty-free withdrawals of principal at any time and for any purpose. The earnings portion, however, must be spent toward qualified higher education expenses. Any leftover funds withdrawn will incur federal income tax and a 10% penalty.

Talk to your advisor to see if 529s are the right way for you to give the gift of education – whether it's for a child, grandchild, family friend or even yourself.

Sources: The College Board, savingforcollege.com, kitces.com, forbes.com

Earnings in 529 plans are not subject to federal tax and in most cases state tax, as long as you use withdrawals for eligible college expenses, such as tuition and room and board. However, if you withdraw money from a 529 plan and do not use it on an eligible higher education expense, you generally will be subject to income tax and an additional 10% federal tax penalty on earnings. An investor should consider, before investing, whether the investor's or designated beneficiary's home state offers any state tax or other benefits that are only available for investments in such state's qualified tuition program.

Not only can giving the gift of education help others, but it can help reduce your tax impact and benefit your overall estate.

While traveling in Michigan seeing some institutional accounts, and speaking at events for our advisors and their clients, I got the chance to reread some emails that have gotten lost in the over 2500 emails that populate my inbox. One such email was from the sagacious Paul Siluch on passive versus active investment management. He scribed this excerpt (as paraphrased:

In large part, this [passive investment trend] is due to the fee advantage low-cost index funds have over active managers. Another factor, though, is just due to money flows. A huge amount of money is now chasing the indexes, which sends them even higher. According to The Wall Street Journal, $429 billion was invested in index funds in 2016 while $285 billion was removed from actively managed mutual funds. . . [However] This is just 9% of all listed stocks. There are over 5,300 publicly listed stocks on U.S. exchanges (source: Financial Post). This means we are pumping most of our money into just a handful of all available stocks and ignoring the rest.

Andrew and I have written extensively on this point suggesting when stocks are undervalued, and the indices are going up, you want to own “Cheap Beta” (passive investment is just fine), but when stocks are neutrally valued you want to have “active management.” We think that is the case here! Intuitively, one has to know that when EVERYONE is “leaning left” you want to “lean right” and clearly everyone is leaning toward “passively investing” currently. In fact, sparked by Paul’s cogent comments, I went back and reviewed my notes from the late-1960s, and early-1970s, regarding the then “Nifty Fifty” (Nifty Fifty). Those of us that are old enough to remember that era know it did not turn out very well; not that we are predicting a similar event here.

Speaking of not turning out right, the Comey firing should not have come as a great surprise. The Republicans will argue Comey was out of control and was violating protocol. The Democrats will claim Comey was getting too close to President Trump’s relationship with Russia. The truth is likely somewhere in the middle. What to watch for now is: 1) Who will the president nominate to run the FBI? 2) Will Rosenstein appoint a special prosecutor? And 3) will Republicans flee from the president over the firing? Whatever the answers to those questions, our models still appear to be on track since they telegraphed this week and next week as probably “quiet weeks” for the equity markets, which should lead to a big “up” move from there. As Andrew said to me yesterday, “Everybody is expecting the stock market to go down, except you and me!” We think the equity markets are setting up for a rally. And that’s the way it is as the Comey caper comes a cropper. Look for some more attempts to pull stocks down into next week, which doesn’t get much traction, and then a slingshot rally should develop. This morning the world is flat once again at 5:00 a.m. here on Lake Michigan . . .

To read more from Raymond James Chief Economist Strategist, Jeff Saut, please click on the link below:

https://raymondjames.bluematrix.com/sellside/EmailDocViewer?encrypt=e1b6b62a-d697-4b45-aa3f-40ef4193e67a&mime=pdf&co=RaymondJames&id=Matt.Goodrich@RaymondJames.com&source=mail

Photo by Tzido/iStock / Getty Images

Article by: PGMI Investments

No matter one’s age, people can have trouble motivating themselves to save for retirement. The most common mistakes that investors make often depend on their life stage – and they frequently relate to human behavior. Simply put, certain behaviors can impede good choices, and our human tendencies can derail even the best intentions.

The Person: Most couples in their 40s have entered their prime earning years, and with the end of tuition bills in sight as their children complete college, they suddenly have more money at their disposal than ever before.

The Behavior: For the human brain, this newfound liquidity could feel like a raise — a.k.a. the perfect excuse to splurge on that new car or timeshare in Hawaii. But now is the ideal time to make up for the undersaving they were doing when life was much more expensive.

The Point of View: According to Robert Stammers, director of investor education at the CFA Institute, the organization that helps chartered financial analysts educate their clients in areas including retirement security, making up for this lost time is particularly difficult when couples have spent decades convincing themselves that this life stage is actually the finish line. “In the back of their mind the entire time they’ve been thinking, ‘If I can just get the kids out of school, then I can buy all of the things I couldn’t afford before,’” he explains. “But that’s a real trap, because now is when they can optimize their retirement savings.”

For that reason, Stammers believes this is the ideal time for such a couple to get disciplined by holding expenses steady. “They have increases in income,” he explains, “so if they’ve set their lifestyle static and live within that, then all of their extra income can be put into a retirement account and start earning returns for the future.”

This is particularly important when one considers retirement liability — the amount of money that people need to amass to live for 30 years in retirement. “For a lot of people, that number is larger than they realized,” says Stammers. “It’s very hard for most people to hit that number if they don’t take the time to maximize savings in their 40s.”

The Data: The temptation to spend newfound money on an extravagant purchase is strong, but now is when to make up for lost time. Take a hypothetical 45-year-old couple that is starting with $50,000 in savings, has an annual household income of $100,000 and plans to retire at 67. If they go from saving 9 percent to 15 percent of their salaries — and receive annual cost-of-living raises that keep pace with inflation — a 7 percent return on investment will yield nearly $350,000 more at retirement

Assumes growth rate of 7% annually. This is a hypothetical example. It is not indicative of any actual investment. There is no guarantee that this will occur and the outcome could differ depending on an individual’s particular situation.

The Change: Using traditional methods, a couple preparing for retirement will spend whatever they’ve budgeted for the month, then save the money that is left over. But Stammers recommends using the inverse approach as a trick to stay on track: save the amount you need for retirement first, and only spend the excess.

Doing so makes saving for the future an active, not a passive, pursuit. “It gets you into this discipline of budgeting and tracking your expenses so that you live within your means and optimize what you save,” says Stammers, who emphasizes the importance of putting away even the smallest amount. “Over time, simply putting capital into the market is going to increase the probability of reaching your financial goal.”

As such, Stammers believes it’s vital to make saving as automatic as possible, and he sees target date funds as a great way to remain goal-oriented — particularly for investors who aren’t confident about managing their own money and play it too safe as a result. “One thing that target date funds do is keep people in something that should give them some return, as opposed to just being in a money market,” he explains. “This has the potential to give them a decent return over the long term. If you’ve got a target date fund, you’ve got a long-term lens.”

While it’s harder to quantify, target date funds can also offer peace of mind. “At the CFA Institute, we say that if you’re having trouble sleeping at night, then you’re either in the wrong products or the wrong portfolio,” Stammers adds. “You should be able to put your money away consistently over time, and not be worried that you’re not going to make it to the end line.”

And if a couple over-saves? Stammers has yet to hear that complaint: “Let’s put it this way. No one is going to get upset by having too much money in retirement.”

Created in Partnership With:

Bloomberg Media Studios

These materials are provided for informational or educational purposes only. The information provided is not intended as investment advice and is not a recommendation about managing or investing your retirement savings. In providing these materials, Prudential Financial Inc, its affiliates and its subsidiaries are not acting as your fiduciary as defined in the Department of Labor’s Fiduciary rule or otherwise. If you need investment advice, consult with a qualified investment professional.

Investing involves risk. Some investments are riskier than others. The investment return and principal value will fluctuate, and shares, when sold, may be worth more or less than the original cost, and it is possible to lose money. Past performance does not guarantee future results. Asset allocation and diversification do not assure a profit or protect against loss in declining markets.

The target date is the approximate date when investors plan to retire and may begin withdrawing their money. The asset allocation of the target date funds will become more conservative as the target date approaches by lessening the equity exposure and increasing the exposure in fixed income type investments. The principal value of an investment in a target date fund is not guaranteed at any time, including the target date. There is no guarantee that the fund will provide adequate retirement income. A target date fund should not be selected based solely on age or retirement date. Participants should carefully consider the investment objectives, risks, charges, and expenses of any fund before investing. Funds are not guaranteed investments, and the stated asset allocation may be subject to change. It is possible to lose money by investing in securities, including losses near and following retirement.

© 2017 Prudential, the Prudential logo, the Rock symbol and Bring Your Challenges are service marks of Prudential Financial, Inc., and its related entities, registered in many jurisdictions worldwide.

Chris Bailey, European Strategist, discusses centrist Emmanuel Macron's election victory over populist Marine Le Pen.

May 8, 2017

"I will respect everyone in their beliefs, I will seek reconciliation because I want the unity of our people. Finally, I will serve you with humility, with strength, in the name of our national rallying cry: Liberté, Egalité, Fraternité." – Emmanuel Macron

Despite the pollsters being wrong – by an even greater margin than on the U.K.’s Brexit referendum result or the U.S. Presidential vote – the centrist Emmanuel Macron garnered just over two-thirds of votes successfully cast for the biggest French presidential vote victory since Jacques Chirac’s 2002 victory against Jean-Marie Le Pen, the father of yesterday’s losing candidate Marine Le Pen.

At one very clear level, Macron’s success is a victory for the continuation of the European ideal. His candidacy has been cloaked in the flag of the European Union and the sharp relief expressed in the messages of congratulations from other European political leaders reflect this. As with the Dutch elections just under two months ago, the forces of populism have politically been unsuccessful in gaining power and pro-European mainstream politicians have another term in office to stimulate faith in pan-European ideals.

France is especially influential in the development of this vision given the country’s size and proud, important history in the creation and administration of the modern European Union and euro single currency project. Without France, neither of these initiatives can properly function and, until recently, it was an accepted fact that the Franco-German partnership at the heart of Europe pushed forward together. The French economic malaise of the last decade has led to high unemployment, suppressed economic growth and internal political angst compared to their erstwhile German partners and has unsteadied the European economic and political ship.

So does Monsieur Macron have a range of insightful answers? At face value, his proposed legislative initiatives (including public investments worth €50 billion spread over five years for environmental measures, apprenticeships, digital innovation and public infrastructure; lowering the corporation tax rate to 25% from 33.3%; and pledging to make material reforms in France’s state pensions and policy of propping up failing businesses) appear to be a step in the right direction. His challenge will be to shape a coalition of sufficiently like-minded interests in the French Parliament – following upcoming elections in a few weeks’ time – to push through such much-needed reforms. Even modest success here could have a cascading positive impact on France’s economic performance and give a vision for other Western European countries trying to revitalise both economic growth and political hope. In investing terms, the big winners in such a scenario would be the currently undervalued euro – which would re-attract global capital flows – and sectors/companies (in retail, construction and banking, for example) with significant euro zone revenues and profits.

As for the Brexit debate, the re-election of mainstream, pro-European politicians may potentially cause problems. However, an un-cohesive, economically hindered and politically failing European Union is likely to be a lose-lose for everyone. Common sense – and a softer Brexit – is much more likely to prevail with a European Union that is feeling better about itself.

The financial markets are not without foresight, however. Inflows into European equities and the euro currency started to turn around earlier this year, and the noticeably positive reaction to Macron’s first round victory two weeks ago will not be repeated after the second round complete triumph. The travelling hopefully period is now coming to a close, and with President Macron's formal arrival in a week or so, reality will have to start kicking in. I still like the relative valuation and opportunities contained within European stock markets, but as 2017 rolls into 2018, you are going to have to increasingly believe that some element of change is coming.

"Reform or die" sounds a bald and provocative observation, but for the French political economy and the broader cohesive euro zone project, it is close to reality. Growth has to be boosted, labour market flexibility enhanced and general productivity/competitiveness levels improved not just in France but in other large swathes of the European Union. President Macron probably has until the end of this year to work out the final details and bring together his effective Parliamentary majority and then he is going to have to start proving up. But if he does, the motivations for others will build. After all, the German supply side reforms of the 1990s or the British equivalent changes in the 1980s historically show that politicians with strong convictions can push through change in Western Europe.

Bonne chance, Monsieur Macron – more than just your potential re-election in five years’ time rests on this.

Photo by designer491/iStock / Getty Images

Read on to learn how 529 plans are more flexible than you may think. They can be set up by anyone, for anyone, and used for a variety of education costs at all kinds of institutions, not just typical four-year colleges.

Myth: Only parents can establish a 529 account for a child.

Reality: Anyone can open and contribute to an account for any beneficiary – no age limits or family connections necessary. Often, grandparents open 529 accounts to help fund college for grandchildren (with the added bonus that their assets won’t be factored into financial aid calculations and they may even benefit from reduced taxes on their estate).

Myth: Once the child is in college, he or she has control of the 529 account.

Reality: The account owner has – and maintains – control of the assets as long as the account exists.

Myth: Contributions to a 529 plan will limit financial aid opportunities.

Reality: While 529 assets can have an effect, it isn’t as significant as the impact of some other educational savings tools. Since 529 assets are under control of the account owner (not the beneficiary), they’re assessed at a maximum rate of 5.64% when determining expected family contribution (part of the financial aid formula). In comparison, investment assets in the student’s name, such as UTMA/UGMA accounts, are assessed at 20%.

Myth: I have to invest in the plan sponsored by the state where I live.

Reality: You can invest in any state’s 529 plan, but look at what your state’s plan offers first since some provide state tax breaks and other benefits to residents. Plans offered by other states may not provide these same benefits.

Myth: If I invest in a 529 plan, the beneficiary is limited to attending a public, four-year university.

Reality: Funds can be used for qualified expenses at eligible educational institutions in the U.S. and even some abroad, including private or public colleges, universities, and technical or vocational schools that qualify for federal financial aid. Check the Department of Education’s website (fafsa.ed.gov) and click School Code Search to find qualifying institutions.

Myth: If it turns out the beneficiary doesn’t go to college or receives a scholarship, all the money I’ve invested is lost.

Reality: Since the owner – not the beneficiary – controls the account, you can change who receives the funds to any eligible family member. Another, although less attractive, option is to take a nonqualified withdrawal. Earnings are then subject to the usual taxes and a 10% penalty (penalty waived in the instance of a scholarship).

Myth: I can’t participate in a 529 plan because my income is too high.

Reality: Anyone can invest. There is actually no income limit to establish or contribute to a 529 plan.

Earnings in 529 plans are not subject to federal tax and, in most cases, state tax, so long as you use withdrawals for eligible college expenses, such as tuition and room and board. However, if you withdraw money from a 529 plan and do not use it on an eligible college expense, you generally will be subject to income tax and an additional 10% federal tax penalty on earnings. Changes in tax laws or regulations may occur at any time and could substantially impact your situation. You should discuss any tax or legal matters with the appropriate professional.